Preparing for a growth equity interview

Growth equity roles are among the most attractive in the investing world right now. Growth investing is attractive because it allows investors to place exciting bets on the future (similar to venture capital), while also bringing rigor and potential for attractive returns (similar to private equity).

However, given the unique nature of growth equity, preparing for growth equity interviews can present many unique challenges and questions for candidates.

Given my experience in the industry – I previously worked as an investor at General Atlantic, and I’ve worked for several years at portfolio company Airbnb – below I put together a prep guide to help candidates ace their growth equity interviews.

In it, I will discuss the most common (and important) interview questions you’ll be asked in growth equity interviews, in addition to the sourcing, modeling, and case studies you can expect.

Growth equity overview

Growth equity refers to investing minority ownership positions in high growth companies that have demonstrated customer traction and have proven, to a large degree, the viability of their business model.

Many find it helpful to think of growth equity investments as the stage after venture capital, but before private equity and hedge funds (LBO buyouts and IPOs, respectively). Unlike private equity buyouts, growth equity investments tend to be minority (sub-50%) stakes and involve little or no debt.

Elite firms from every corner of the asset management industry (e.g. venture capital, private equity, hedge funds, etc.) have raised growth stage funds in order to capture attractive returns.

Further, growth equity investing roles are among the most competitive in the finance world, because they are well-compensated (similar to private equity) and they focus on investing in exciting, high-growth companies.

For an in-depth tutorial, including comparisons to private equity and venture capital, check out this complete primer on growth equity industry, investment strategy, and careers.

How to get growth equity interviews

The ideal qualifications for growth equity roles vary, based on the role/firm you’re interviewing with and the stage of career you’re in.

Most growth equity firms seek to hire candidates with “traditional” finance background – this includes stints in investment banking, consulting, other kinds of investing, etc. However, new or smaller growth firms are more open to hiring candidates with diverse or non-traditional backgrounds as pre-MBA associates (e.g., former entrepreneur, product manager, other industry role).

Below is a summary of the “traditional” qualifications that most growth equity firms look for:

- Undergrad interns and full-time analyst roles – Competitive undergraduate schools with a track record of achievement in extracurriculars, leadership, and finance-related activities; you do not generally need to have studied business or economics, but this may vary based on the firms’ preference

- Pre-MBA associate roles – Former analysts from investment banking and management consulting programs. Given most pre-MBA roles are filled by candidates with just 1-3 years of post-undergrad work experience, one’s undergrad qualifications can also play a role in assessing your candidacy as well

- Post-MBA or partner track role – prototypical qualifications are: (1) experience in investment banking or management consulting, (2) significant pre-MBA experience at a strong investment firm (e.g. private equity, growth equity, maybe venture), and (3) attend a top MBA program

Growth equity headhunters

Many growth equity firms, especially the larger and more established ones, work with traditional headhunters and recruiters to find candidates to interview. Usually the recruiting firm will be hired to provide the growth firm a list of pre-vetted candidates, from which the growth equity firm will ultimately decide who gets an interview.

Usually headhunters will generally reach out to candidates proactively in the months leading up to recruiting seasons, if they have an investment banking or consulting job.

Growth equity networking

While it’s unlikely to “get” you the job, networking can be pivotal in getting you an interview. This, of course, depends highly on the firm and the situation, but when done well, it can help you get opportunities.

The hardest part of networking is usually that it can be difficult to get engagement from growth equity investors, given how busy they are and how many candidates reach out. To help candidates navigate these and other challenges, I’ve created a separate guide that goes into lots of detail about how to network successfully in growth equity; check it out for more details.

Growth equity interview process

Depending on the firm, recruiting for growth equity can either look like private equity recruiting (highly structured process with a defined “on cycle” recruiting schedule) or venture capital recruiting (less structured process with more “off cycle” opportunities).

Multiple rounds

Regardless of on-cycle vs. off-cycle, a typical interview process usually spans several rounds of interviews, no matter the role. Processes often start with an initial phone screen, generally conducted by an associate or VP-level person at the firm. If a candidate makes it past the initial screen, he or she would move to superday interviews (typically, a batch of interviews conducted on a single day).

If the candidate makes it through the superday, they would likely be assigned a case study assignment (check out my guide on growth equity case studies for more detail), and they might be invited back for an additional superday round of interviews.

Whereas the first superday round is likely to be administered by VP and principal-level professional, the final superday is much more likely to involve group heads, managing directors, and partner-level folks for one or more of the interviews.

Getting an offer

After completing your final round of interviews, firms will usually make a decision as to whether to give you an offer relatively quickly (e.g. in a matter of days). Having been part of this before, I can tell you that usually the bottleneck that prevents firms from making decisions faster is the difficulty in coordinating across all interviewers’ busy schedules to find a time to huddle and make a decision.

During on-cycle recruiting, firms generally make decisions very quickly, sometimes on the same day, in order to be competitive with other buyside firms making offers.

Growth equity interview prep

One of the most difficult aspects of preparing for growth equity interviews is the sheer variety of material one might encounter during interviews and therefore must study during preparation.

While private equity buyout interviews have become mostly standard at this point (e.g. LBO modeling case study + paper LBO, etc), the interview processes at growth equity firms can vary widely. The type of interview you face is usually influenced heavily by the background of the firm; for instance, if the firm has venture capital roots, your interview with the growth fund may not only cover typical growth material, but it may also borrow interview elements that are more common to traditional venture interviews.

Given the diversity of firms now investing in the growth stage (e.g. firms with roots in private equity, venture capital, hedge fund, asset management, etc.), the material one could face in growth interviews is quite vast.

The good news is this creates an opportunity for diligent candidates to set themselves apart by undertaking a structured and comprehensive interview prep plan.

In the next sections, I will provide an overview of major areas to prepare:

- Why growth equity

- Interview questions

- Modeling test & other case studies

- Mock cold call exercise

- Market thesis exercise

- Other prep areas

Comparing prep to private equity and venture capital

Relative to private equity interviews, growth equity interviews tend to place a greater emphasis on assessment of markets, sourcing & cold calling, and growth modeling techniques. While you need to know LBO modeling (including paper LBO), it’s unlikely you’ll receive questions on advanced LBO modeling tactics.

Relative to venture capital interviews, growth equity interviews tend to place more weight on modeling case studies and rigorous financial analysis. Meanwhile, in venture interviews, you will likely encounter more questions about early stage investing and term sheet understanding. In both types of interviews, you will be expected to discuss markets, trends, and businesses that are attractive to invest in.

Why growth equity

Growth equity interviews tend to be heavy on assessment of “fit”. One major aspect of “fit” is whether you have a clear and compelling rationale to why growth equity makes sense as the next step in your career.

There’s good news though. As an industry, growth investing has such a compelling story that it shouldn’t be hard to nail this part of the interview if you put in some work up front. I mean, think about it, the entire industry is about finding and helping the next generation of companies that will change the world. That’s certainly much more exciting than doing leveraged buyouts of slow-growing plastics companies in traditional private equity :-).

Still, there are more nuanced layers of this answer to consider. For example, how does your experience prepare you for growth equity and what skills are you looking to develop in growth equity that you couldn’t develop in other kinds of investing? You’ll want to be prepared for these and other areas in case your interviewer wants to go deeper.

Luckily, I’ve prepared an in-depth guide to help you answer the question “why growth equity”; check it out for more detail.

Growth equity interview questions

Of course, all interviews come down to a series of interview questions. As with any interview, what questions you receive will depend highly on not just the firm, but also on the individual interviewer.

Before we get to interview questions & answers, I feel compelled to give a public service announcement. I know many readers won’t believe me, but you should practice not only WHAT you say, but HOW you say it. The substance of your answers is clearly very important, but don’t underestimate the importance of your delivery and other non-verbal communication (i.e. your overall impression, posture, etc.).

In growth equity, you will be representing the firm with investment targets from the get go, and so firms place a high importance on how well you communicate and carry yourself in interviews.

Alright, with that general advice, let’s talk about actual growth equity interview questions. Generally, interview questions in growth equity will fall into these categories:

- Standard fit questions

- Behavioral questions

- Resume and deals questions

- Technical questions

Different firms and interviewers will prioritize categories differently; however, as a general rule, I find that candidates are consistently surprised by the extent to which their interviews seemed to focus on standard fit and behavioral questions. Of course, you will still need to prepare for all question types (e.g. technical & investing) — because a bad answer can certainly be disqualifying — but don’t be surprised if the normal fit and behavioral questions take the majority of your interviews.

To a degree, answering these fit and behavioral questions should be similar to interview experiences for other jobs. However, I find that successful candidates for growth equity roles are able to infuse their answers with evidence of key traits that growth firms are looking for: self-starting / entrepreneurship, ability to learn quickly, love for investing, and track record of excellence.

To see examples from each interview question category, check out my deep dive on non-technical growth equity interview questions (including suggested answers).

Growth equity technical questions

Technical questions are a source of lots of anxiety for candidates. It’s understandable; technical questions are more black-and-white than other forms of interview questions. There’s (usually) a right and wrong.

I find there’s also general confusion about technical questions as they relate to growth equity interviews. The reasoning goes: if growth equity doesn’t have complicated debt and LBO structures, then what is there to ask about?

Well, the answer is growth equity technical questions tend to fall into these buckets:

- Growth investing concepts

- Accounting concepts

- Deal structuring & term sheet concepts

If you’d like to go deeper and review sample questions with answers, I discuss growth equity technical questions in a dedicated article. Check it out!

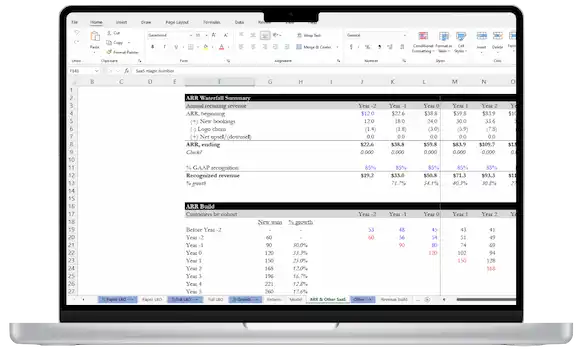

Growth equity modeling case study

Many growth equity interview processes will require candidates to complete a modeling test or case study as part of interviews. This can occur in the office or as a take-home assignment, but in either it will be time limited. Typically, it involves building an investment model and developing an investment recommendation on a target company, based on materials provided (e.g. memo or presentation).

Compared to private equity interviews, the modeling itself tends to be much less likely to have tricky or advanced LBO concepts (e.g. PIK debt, etc). Instead, it’s likely the modeling exercise will require modeling features that are more specific to growth phase deals (to name a few: minority investments, primary vs. secondary proceeds, employee options, detailed revenue builds, SaaS and other software specific features). That said, many growth equity firms – especially those with more of a private equity orientation – will still ask candidates to build or discuss a basic or paper LBO model to ensure they grasp the fundamentals of modeling.

In addition to building a model, the modeling case study in growth equity tends to put more importance on the quality of the candidate’s investment recommendation, which the model will support. These recommendation usually involve preparation of written materials (e.g. memo, slides) or spoken presentation.

Overall, candidates should be comfortable with the following in order to be fully prepared:

- 3-statement model with debt schedule

- Paper and basic LBO model

- Growth technicals/modeling

- Software specifics

- Investment recommendation

For a detailed breakdown at what you need to know for each of these areas, check out my deep dive into growth equity case studies and modeling tests.

Mock cold call exercise

Especially in a junior role (e.g. pre-MBA or post-undergrad), finding and contacting new investment prospects is usually a central part of your job in growth equity (via cold calling).

The emphasis many firms place on the skill of cold calling is one of the most unique elements of growth equity recruiting. Given its importance on the job, many growth equity firms will screen heavily for cold calling during interviews, especially for junior roles.

While some firms will simply ask about your experience and attitudes toward cold calling during interviews, some firms assign such an importance to it that they will have an entire activity or case study dedicated to it. In general, this exercise will be an explicit interview where you “role-play” with your interviewer who pretends to be the CEO of an investment prospect in a mock cold call.

In the mock cold call, you pretend you work for the investment firm and you introduce the firm to the “CEO” while also asking questions to learn more about the business and assess the investment prospects. Afterward, you usually end the “cold call” conversation, and then do a “mock debrief” where you report on your conversation to you deal team (again, played by your interviewer).

To go even deeper on mock cold calls and potential interview questions about them, check out the complete guide I wrote on growth equity cold calling.

Market thesis exercise

I’m a nerd, but if you were to ask me what my favorite growth equity interview activity is … I’d say it’s the market thesis exercise (and it’s not even close)!

The market thesis involves the firm asking candidates to present an investment thesis on a particular market or trend that’s attractive. In addition to investment catalysts (why now), the candidate should be ready to discuss market size, growth trends, leading companies, pros and cons of business models, and public valuation metrics. Also, the candidate should prepare 2-4 private companies they think are attractive that may be “investable.”

The reasons I love this activity so much is: (1) it provides candidates a chance to outshine their peers, (2) it’s meritocratic because this is the actual job of a growth investor. Plus, it’s fun! You get to have a view on where the world is going and how to invest behind those trends.

The market thesis exercise can either come up as part of interview conversation (e.g. tell me about a space you like), or some funds give it as a formal take-home assignment where the candidate prepares a formal presentation of slides.

Stock pitch & other investment ideas

In addition to the market thesis, firms are likely to probe your investment judgement and ability to present investments in a number of other ways:

- Stock pitch – this is definitely the most common; candidates should come prepared with 2-3 public companies they are prepared to pitch as an investment

- Firm’s portfolio company – it can be a little unfair, but sometimes firms ask candidates what portfolio companies of theirs that you like (and don’t) as investments; candidates should do (light) prep beforehand to find one you like and one you don’t

- Your deals – even if the transaction is not an acquisition (e.g. debt financing), be prepared to speak about each deal company as if it were an investment. Would you invest? Why or why not?

To go even deeper, check out my guide to preparing a stock pitch or investment idea for interviews.

Miscellaneous prep

Alright, so we’ve covered the major areas of preparation. You’re nearly ready. But there’s still some odds-and-ins we haven’t covered above that you’ll need to prep:

- Review the firm and interviewers – During your preparations, hopefully you’ve already studied the firm, its portfolio companies, and who you will be interviewing with

- Prepare 4-5 questions to ask the interviewers – You’ll get time to ask questions of your interviewers, so make sure to consider what you want to ask ahead of time; we discussed this in more detail below

- Print fresh copies of your resume – Print out way more copies than you think you need. If you have 5 interviews, print at least 15 copies. It’s possible some of your interviews will be 2-on-1, and you’ll still have some to spare.

- Don’t over-caffeinate – When I was interviewing for growth equity roles, I remember at one point my voice started shaking, because I was over-tired and over-caffeinated. Remember that you will have lots of natural adrenaline without over stimulation from caffeine

- Bring a nice folder with notepad and pen – Especially during Q&A at the end, you may want to play the “studious” interviewee by taking notes. Even if not, this gives you something to keep your resumes in.

- Practice, practice, practice (talking) – Before every key interview, I spend at least 30 minutes practicing answers out loud just to get the right energy flowing

Conclusion

Alright, that’s it for now. If I missed any topics, feel free to email me at growthequityinterviewguide@gmail.com. Also, check out my other free articles, and if you want to go even deeper, take a look at my comprehensive interview preparation course.

Break Into Growth Equity

Break Into Growth Equity