Preparing for private equity or growth equity interviews is quite an undertaking. Whether it’s your first interview or your tenth, there’s a lot you need to prepare.

Preparing for that first one is especially tricky, though, because you’re facing your first paper LBO exercise.

The paper LBO requires knowledge of the ins-and-outs of a leveraged buyout model, as well as strong analytical skills, knowledge of the deal, and a quick mind for mental math.

Once you know how to do it, be sure to practice – you don’t want to have the additional challenge of feeling pressured while you think.

In this article, we’ll cover what a Paper LBO model is, how to prepare, and example prompts so you can go into it feeling extremely confident.

What is a paper LBO?

At its most basic level, a paper LBO highly is a simplified LBO model that uses certain simplifying assumptions that allow you to either calculate using pen and paper (or verbally). It allows you to estimate returns for a deal quickly without a full model.

The paper LBO is not actually used much “on the job” but it is often asked for during private equity interviews (and even growth equity interviews).

In an interview situation, the interviewer will commonly ask the candidate to pencil out a paper LBO for a company or deal they’ve worked on in their previous job. In other cases, the interviewer might present a new company and supply the candidate with assumptions and financial metrics to use.

Because the paper LBO simplifies the math, usually you can complete a paper LBO using paper & pen, or verbally in an interview. Sometimes interviewers will lead you along with questions, as you complete the Paper LBO live on the fly.

Usually the paper LBO exercise will last 5-20 minutes during an interview.

Paper LBO in Interviews

Paper LBO calculations are mostly for private equity interviews, although they can show up in growth equity interviews as well.

The Paper LBO assesses many key skills for private equity and growth equity jobs and internships:

First, it’s an excellent way to quickly assess your knowledge of the mechanics of LBO modeling.

It’s also a great way for an interviewer to assess your communication and quantitative skills. Can you make quick calculations on the fly? Can you sift through financial metrics in your head and calculate orally with confidence?

Additionally, the Paper LBO allows the interviewer to dig into a deal on your resume by asking you to sketch out a Paper LBO for the deal. This allows in-depth follow up questions.

Finally, because usually the Paper LBO is requested for a company/deal you’ve worked on, it tests your level of preparation for the interviews, because in order to complete it successfully you need to remember or memorize key financial metrics for the company and deal.

Paper LBO vs full LBO model

The paper LBO you might encounter in an interview is a highly simplified version of a full leveraged buyout model.

Here are a couple key ways that paper LBO models differ from full LBO models:

- Instead of building a full 3-statement model, simply focus on projecting Revenue, EBITDA, and free cash flow every year (memorize these for the entire projection period for all your deals!)

- Since you are memorizing financial numbers for Revenue, EBITDA, and FCF, it’s OK to use figures that are rounded to the nearest $5 million

- Often, you’ll assume growth in metrics over the projection period is linear, allowing you to memorize the year 0 and year 5 metric values (and assume linear growth between them)

- No need to build out balance sheet or debt schedule; you’ll capture their impact by simply projecting FCF

Sometimes interviewers will throw in a complicating factor or two, but the calculations are all designed to be completed without a computer in less than ~20 minutes.

Step-by-step process for Paper LBO

In many ways, completing a paper LBO is the same as completing any other financial model.

For any model, you can remember the ASBICIR process. This stands for the following steps:

- Assumptions – gather all your operating and entry assumptions (incl. pro forma valuation and debt figures); start with the purchase price and debt/equity financing split.

- Sources and uses – using the assumptions, fill out your sources and uses, which shows where the cash flows to and from in the acquisition transaction. Ultimately, this will get you to your “Sponsor Equity” which is the investment amount upon which you should base your IRR

- (Pro forma) Balance sheet – With your Sources & Uses done, you can now complete your pro forma balance sheet, and start laying the foundations for projecting it forward until the exit year. This includes setting up your debt schedule, if your modeling an LBO

- Income statement – next, you can start projecting forward your income statement, all the way down to net income; notably, do not yet integrate interest expense; leave this blank for now

- Cash flow – with your income statement and balance sheet up, you can project forward your cash flows. This and the prior two steps will be iterative as you set up schedules and make calculations that are interdependent on multiple statements (e.g. D&A)

- Interest – finally, once your 3-statements are connected and projected forward, always the last step is to calculate interest expense and connect it to the income statement; turn on model iterations

- Returns – the last step is to make an assumption about your exit, and to calculate your returns by comparing the entry investment amount to the exit investment amount

For the paper LBO, the only differences are:

- No need for Balance Sheet and Interest Expense steps; these are both excluded; given this, you’re left with the Paper LBO short version: ASICR

- Instead of building a full 5-year projection, instead build up the model for Year 0 and Year 5 (from memory). To estimate the intervening years, you can either assume linear growth or you can use the “average” method

- To estimate the debt balance at exit (year 5), take the average of Year 0 FCF and Year 5 FCF. This will give you average FCF across all 5 projection years. Then take this number and multiply it by 5. This is an estimate of the total amount debt will decrease during the hold period

- Round numbers to the nearest $5 million

Paper LBO format

Sometimes your interviewer will give you calculation aids like a calculator or basic Excel functionality (which you shouldn’t count on).

However, most of the time your interviewer will want to hear you talk through your thought process. After all, they are hiring human talent, not a calculating robot. (AI isn’t coming for private equity – yet.)

Follow the ASICR flow above as you calculate and speak.

Plan anywhere between 5 and 20 minutes for total exercise time, both calculating and speaking.

As you practice, record yourself going through the entire thing, both to time yourself and to assess your confidence and speaking ability.

Paper LBO Example

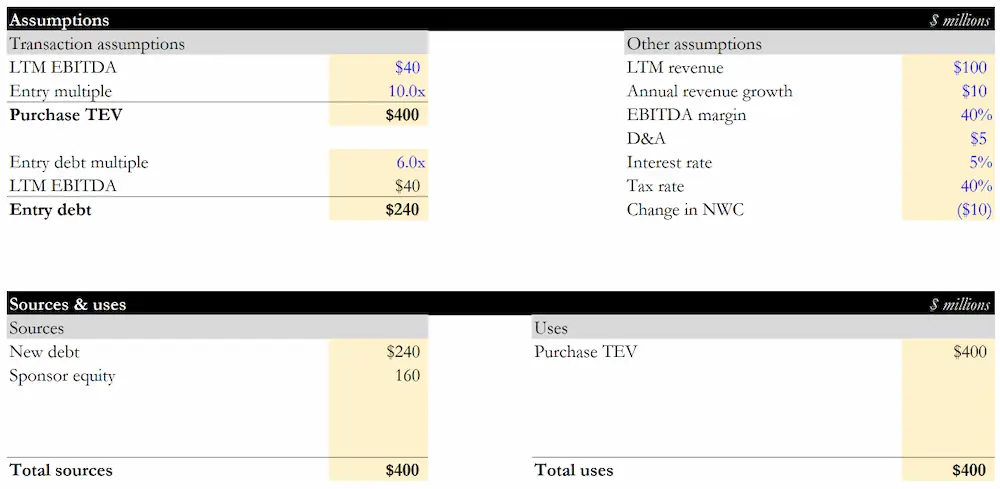

This is a sample paper LBO prompt you might be given in an interview situation.

The assumptions here are pretty standard, but if there are any different ones in your interview, you will know about them. The final result of your paper LBO calculations will be the IRR and MoM for the deal.

Here’s the sample prompt:

Imagine our firm is considering an LBO of Company X, and you’re on our investment team. Right now, create a paper LBO live with your interviewer to estimate the IRR and Multiple-on-Money return for the deal. Use the following assumptions:

All dollar amounts are in millions.

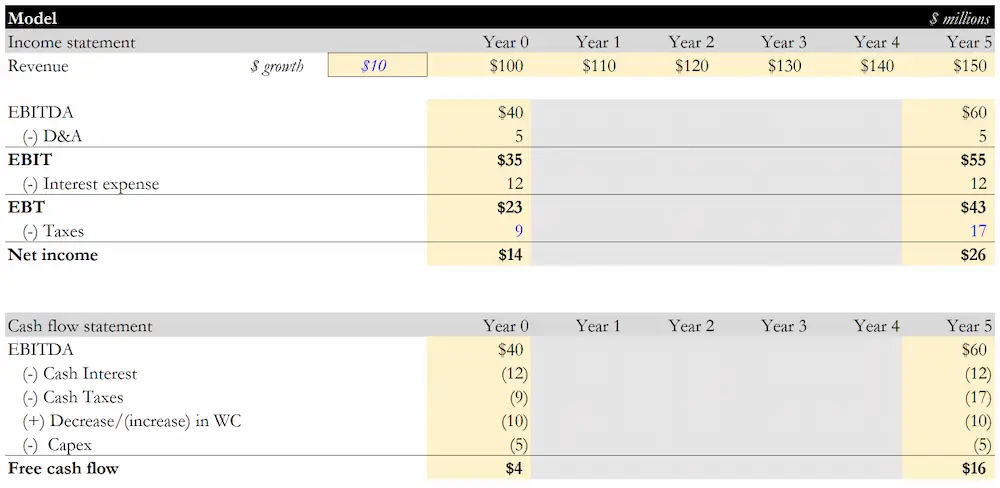

- Year 0 revenue: $100

- Revenue growth: $10 every year

- Year 0 EBITDA margin: 40% in Year 0

- EBITDA margins: remain constant every year

- Entry timing: at end of Year 0

- Entry multiple: 10x LTM EBITDA

- Pro forma debt: 6.0x LTM EBITDA with blended average interest rate of 5%

- Year 0 D&A: $5, flat across projection

- CapEx = D&A throughout projection

- Working capital: Cash investment of $10 every year

- Tax rate: 40%

- Entry timing: at end of Year 5

- Assume entry-exit multiple parity

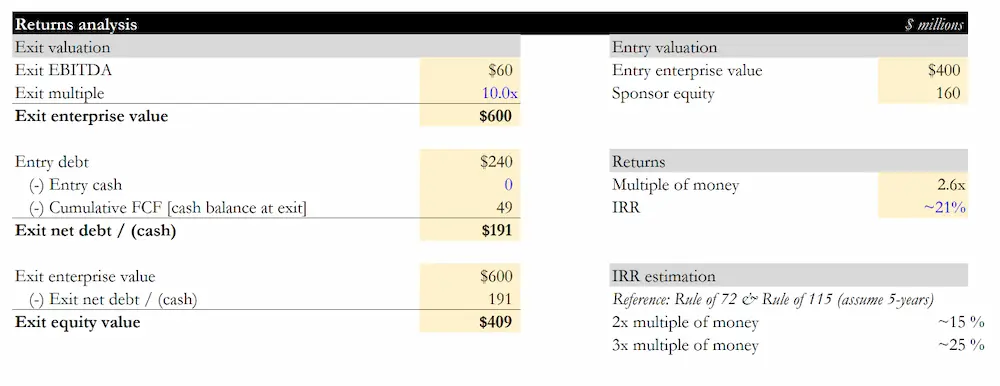

When you pencil out this Paper LBO, what IRR do you get? I get ~21% or 2.6x MoM.

Below are the key steps with outputs.

Step 1/2: Assumptions + Sources & Uses

Steps 3/4: Income & Cash flow Statements

Step 5: Returns

Special tricks for solving

- Follow the flow. The interviewer wants to see that you know how to think like an investor, and wants to see a clear, logical train of thought from beginning to end. Logical shortcuts are fine, as long as the interviewer can follow what you are doing.

- IRR is tough to calculate, but the multiple on money, or cash-on-cash return, is easy to calculate. You will need the beginning and ending equity values for the company. Then, you can use this to help you find IRR.

- Since IRR involves time value of money, it’s tricky to find without Excel or a calculator. A good rule of thumb is the Rule of 72. The Rule of 72 states that the time it takes to double your money is 72 divided by the MoM rate of return.

There are also IRR tables you can memorize for common IRR values over a 5-year horizon, but the Rule of 72 has the advantage of being more flexible and easier to remember.

Paper LBO prep plan

Private equity headhunters and interviewers alike are looking for one thing: expertise.

Since the paper LBO calculation is one of the most technical things you will cover in your interview, it is worth your while to practice. Timing yourself is also key.

Memorize key deal financials

For each of the major deals you list on your resume, memorize the following financial metrics:

- Revenue- Year 0 (entry) and Year 5 (exit)

- EBITDA – Year 0 and Year 5

- FCF (calculated from EBITDA) – Year 0 and Year 5

- Entry valuation multiple

- Entry debt

- Exit valuation multiple

- Exit debt

- IRR & MoM of deal

If the deal wasn’t an LBO or acquisition, you should still memorize these figures because you might be asked to pencil out an LBO for it anyway.

Memorize the Rule of 72 and Rule of 115

These will help you go from multiple on money to IRR calculations for a 5 year period.

Practice with pen and paper

If you are working from pen-and-paper case studies, see if you can get your time down to 5-10 minutes for a straightforward case study, or 10-15 for a more complex example (e.g. read more about private equity case studies).

Practice with your deals

You can also use deals on your private equity resume to generate paper LBO calculations. Go through each deal you completed and create a paper LBO scenario.

Basically, you need to reduce the full model from the actual deal to a simplified paper calculation. Ensure that the relevant ending metrics, such as the internal rate of return and the cash-on-cash return, are the same between the original and simplified versions (within rounding error).

Since it has more meaning to you than a case study, you should be able to memorize each paper LBO scenario for previous deals. Not only will this help you become more efficient with your paper LBO calculations, but it will also make you a more confident interviewee.

FAQ: How long should a paper LBO take?

A simple case study with pen and paper provided and no complicating factors can be completed in five minutes.

A more complex calculation where Excel is allowed should not take more than five minutes either.

If the LBO study has complicating factors like multiple investors or a one-time cash outflow within the case study timeline, it can take longer, but no more than about 20 minutes including discussion time.

FAQ: Are paper LBOs actually on paper?

Yes! Sometimes.

They can be on paper. Some firms may choose to do a simplified Excel version for more complex LBO examples.

Other firms may have paper or may simply do a fully verbal interview with a simpler example.

Break Into Growth Equity

Break Into Growth Equity